- Fiscal.ai

- Posts

- 🗞 Value Play or Value Trap? The 10 Worst Performing Stocks YTD

🗞 Value Play or Value Trap? The 10 Worst Performing Stocks YTD

Sifting through the 10 worst performing stocks in the S&P 500 YTD.

Braden Dennis & Ryan Henderson

April 26, 2026

Written by: Ryan Henderson & Braden Dennis

Happy Sunday! 👋

Today we’re “sifting through the wreckage” and taking a look at the 10 worst performing stocks in the S&P 500 year-to-date.

Let’s dive in!

Featured Story

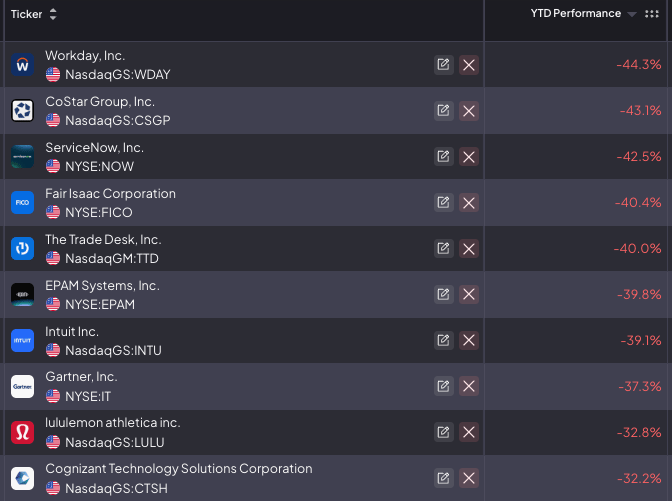

The 10 Worst Performing Stocks in the S&P 500 YTD

In his earlier years, Warren Buffett used to famously scour the 52-week lows list looking for new opportunities.

In the same spirit, today we’re doing some bargain hunting of our own. We’re taking a look at the 10 worst performing stocks in the S&P 500 YTD to see if there’s any attractive opportunities popping up.

Source: Fiscal.ai Dashboard

If you’ve ever applied to a job at a large company, chances are you’ve used Workday.

Over 65% of Fortune 500 companies use Workday as their primary system for HR and finance, with one of the most commonly used features being Workday’s applicant tracking system. Workday is a relatively new entrant to the enterprise resource planning market, but they’ve been a consistent market share taker over the last two decades thanks to being the premier cloud-only solution for human capital management.

If you were looking purely at the trailing financials, you’d probably be shocked to find out that Workday is the worst performing stock in the S&P 500 this year. Workday has now delivered double digit revenue growth every single quarter since coming public (50+ consecutive quarters).

However, markets are forward looking, and the “SaaSpocalypse” has made investors fearful of owning any software stocks over worries of AI disruption. The logic being two-fold: 1) More companies will use tools like Claude or OpenAI Codex to replicate certain Workday features on their own. And 2) if an AI agent can handle HR tasks and payroll, companies may need fewer humans. Since Workday operates on a seat-based pricing model, this would be a headwind to revenue.

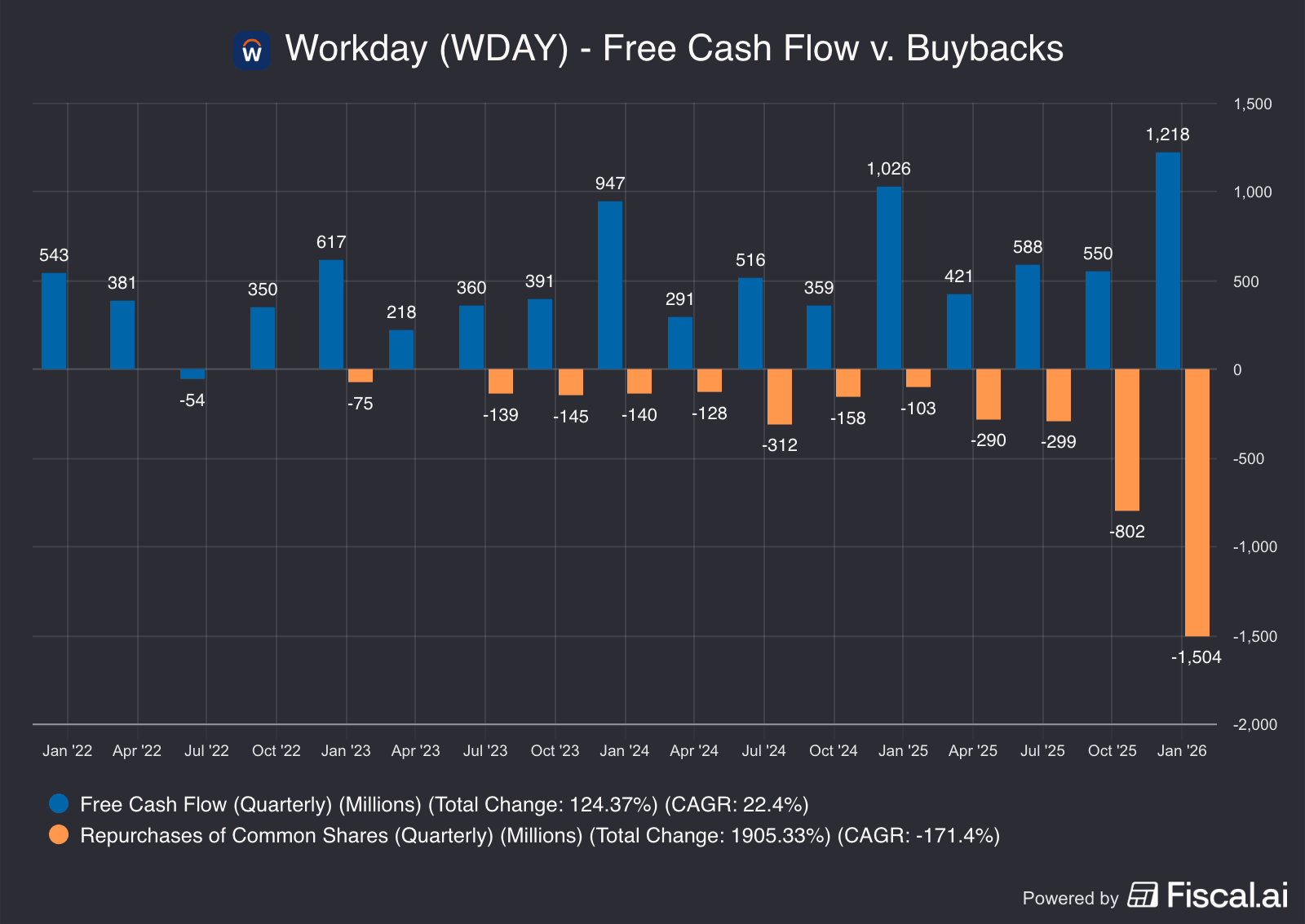

With the stock now trading at its cheapest multiple ever, management has made their opinions on the valuation clear with their capital allocation. Over the last two quarters alone, Workday has spent $2.3 billion on share buybacks which is equivalent to 7.7% of their current market cap.

EV/EBIT: 40.3x

5yr Revenue CAGR: 17.2%

Founded in 1987, CoStar Group has been the undisputed leader in commercial real estate data for several decades. They have a massive army of researchers who track every detail of commercial properties from ownership details to rental prices to lease duration, etc. If you are a serious commercial broker or real estate bank, you almost have to pay for CoStar.

Over the last 5 years the company has been shifting away from its core bread-and-butter commercial business and instead have been investing heavily in the residential space. They acquired Homes.com in 2021 for $156 million and over the last few years specifically have been plowing money into the business.

For the first time since the Great Financial Crisis, CoStar’s free cash flow flipped to negative in 2025. This attracted a number of activist investors including Daniel Loeb’s hedge fund Third Point as well as D.E. Shaw. Both firms have launched public campaigns to curtail over spending on the residential side of the business, and their efforts seem to be bearing fruit. In March, CoStar agreed to reduce its investment in Homes.com by $300 million for 2026.

If CoStar can continue to grow its commercial business while improving its losses on the residential side, investors should see significant margin expansion beyond 2026.

EV/EBIT: N/A (unprofitable)

5yr Revenue CAGR: 14.4%

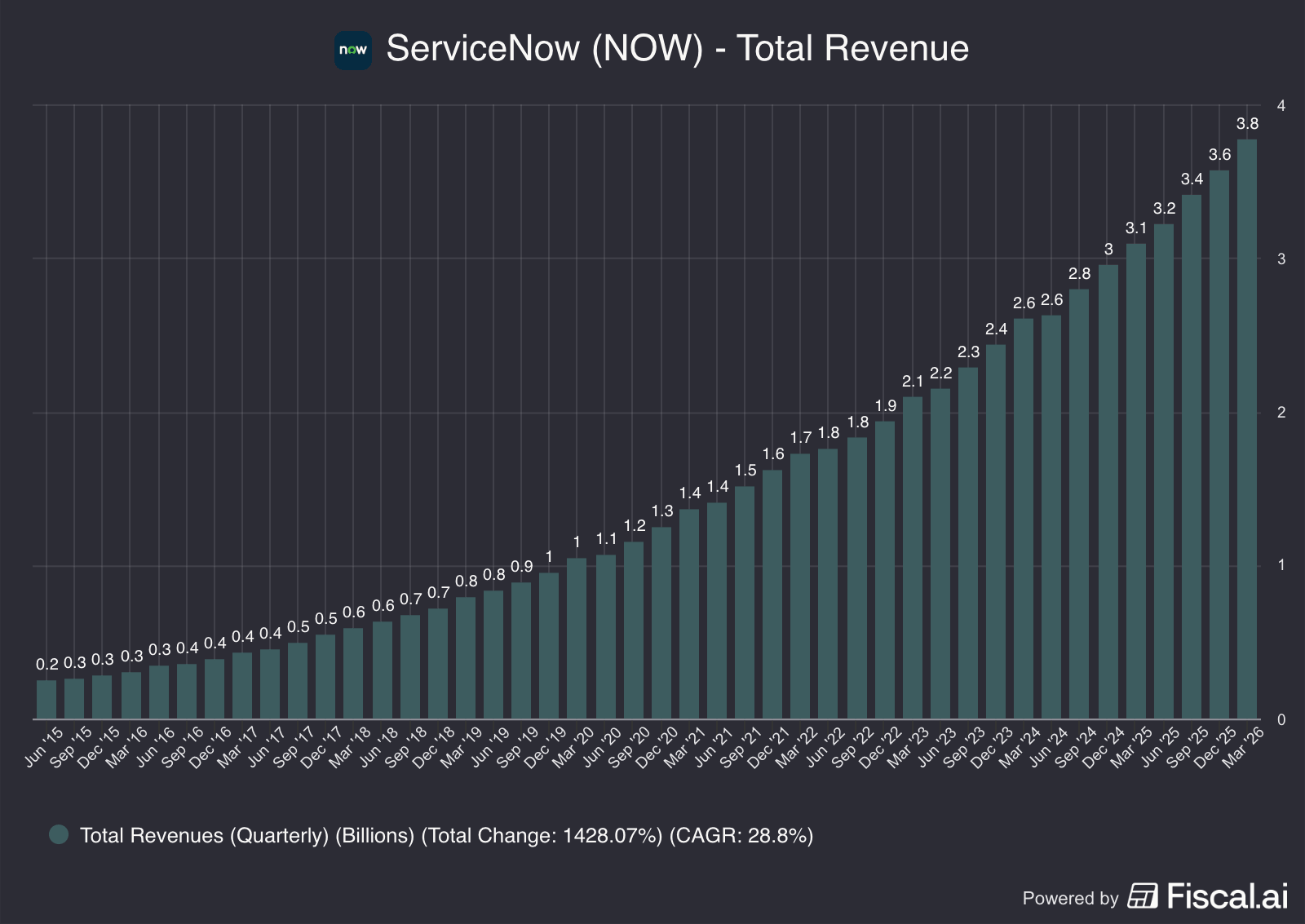

ServiceNow is one of the largest enterprise software companies in the world. The “Platform of Platforms” works with more than 85% of Fortune 500 companies by helping consolidate workflows across different departments into a single cloud platform. Like every other seat-based software company, ServiceNow’s stock has suffered since the rise of AI (now down 63% from highs).

ServiceNow reported 1st quarter earnings this week, and at first glance the numbers looked pretty good. They maintained a 97% customer renewal rate, average contract values grew, and remaining performance obligations jumped 25% compared to a year prior — all in line with or ahead of expectations.

However, investors were instead focused on one issue, margin compression. Between higher than expected integration costs from their Armis acquisition, and the infrastructure buildout associated with their new “Now Assist” AI features, gross margins have dropped from 80% to 75% over the last 2 years.

Shares of ServiceNow are now down 53% since CEO Bill McDermott said the following:

“It used to be the Mag7. Now there's a new category. I'm calling this the Super 8. That's the Mag7 plus ServiceNow. That's right, the Super 8.”

EV/EBIT: 46.3x

5yr Revenue CAGR: 22.5%

In 2022, the US Federal Housing Finance Agency (FHFA) announced a new mandate that approved two new credit score models, the FICO 10T and VantageScore 4.0.

By approving the VantageScore, the FHFA intended to increase competition and break FICO’s long held monopoly in the mortgage lending space. Instead, what it did, was it opened the door for FICO to raise prices considerably.

Since that mandate, the estimated royalty for a FICO mortgage score jumped from $0.60 to $10.00+. So, in the span of a few years, FICO literally increased prices by more than 1,000%!

Unsurprisingly, this has worked wonders for FICO’s profit margins, which have more than doubled since 2020 (23% to 47%) despite an extremely weak housing market. However, this has also drawn significant criticism from regulators, and many investors now fear that these aggressive price increases may trigger the need for federal price caps.

This regulatory headwind has resulted in FICO’s valuation dropping by more than 60% over the last 5 months.

EV/EBIT: 26.8x

5yr Revenue CAGR: 11.1%

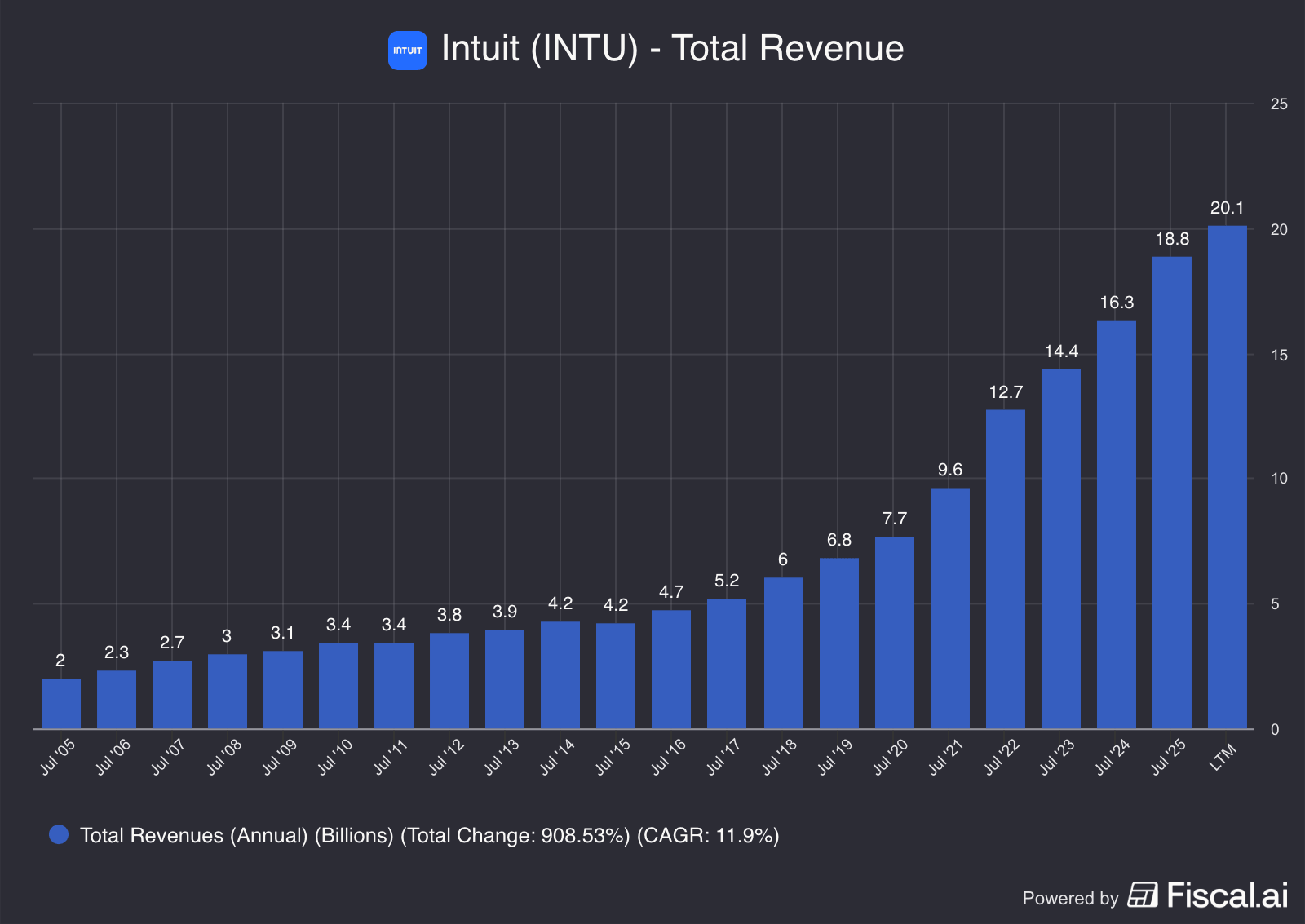

Intuit, the parent company behind TurboTax and QuickBooks, has been one of the best software stocks to own over the last 20 years.

With individuals and businesses uploading their financial data over many years, there is an embedded stickiness to both the TurboTax and QuickBooks software. Even if Intuit raises prices, the switching costs are quite high the longer that you’ve worked with either system.

Given Intuit’s critical position in the financial lives of both individuals and small businesses, investors have rewarded them with a premium multiple. Their average EV/EBIT over the last 10 years has stood at ~40x.

However, with the rise of new AI tools, tax filing software has been a logical target for new startups. For example, Perplexity (a Fiscal.ai partner, btw!) recently launched a new feature within Perplexity Computer that helps users prepare their federal tax returns. On top of the threat from new competitors, the IRS Direct File program was significantly expanded in 2025, with reports suggesting that Intuit lost nearly 2 million users to the free federal system.

In response, Intuit’s management team has launched a new direct partnership with Anthropic to integrate Claude’s models directly into their own systems and they’ve begun accelerating their buyback program.

EV/EBIT: 20.8x

5yr Revenue CAGR: 16.8%

The Trade Desk (TTD) was a fan favorite among growth investors for the better part of the last decade. From its 2016 IPO to Jan. 1st, 2025, TTD generated a total return of 3,805%.

The demand side ad-tech platform told a great story. In an advertising industry controlled by only a few tech giants, The Trade Desk was seen as the “anti-walled garden” and they had the numbers to back it up. From 2015 to 2025, The Trade Desk grew revenue from $114 million to $2.45 billion, totaling a whopping 41% compounded annual growth rate.

However, this year, that positive narrative hit a wall after some of the world’s most powerful advertising agencies publicly turned against them. Publicis Groupe, which is one of the largest advertising agencies in the world and accounts for more than 10% of TTD’s revenue, sent a memo to all of it clients in March advising them to stop using The Trade Desk’s platform after an independent audit found that TTD was applying unauthorized fees to clients without their consent.

Shortly after the Publicis memo, two other advertising giants (WPP and Dentsu) reportedly withdrew from TTD’s direct-to-publisher buying initiative called OpenPath. And to make matters worse, after just 5 months on the job, Alex Kayyal resigned as TTD’s CFO earlier this year.

With a barrage of bad news and sentiment at an all time low, one bright spot for investors would be the CEO’s recent insider purchase. On March 5th, CEO Jeff Green bought $150 million worth of stock on the open market.

EV/EBIT: 17.5x

5yr Revenue CAGR: 22.7%

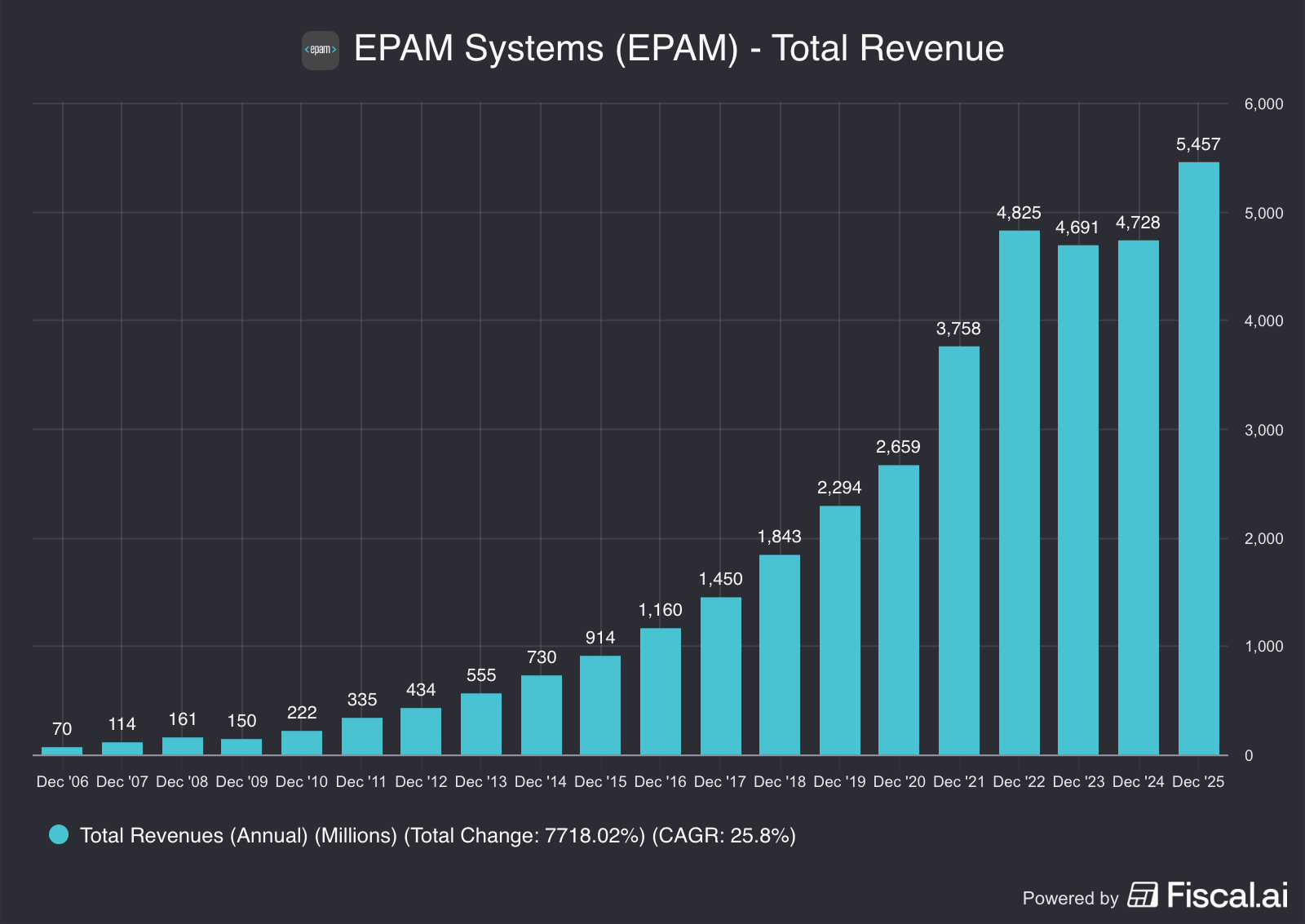

The last 3 decades have been phenomenal for EPAM Systems.

Founded in 1993, the IT services firm has helped connect the massive (and underutilized) engineering talent pool in Eastern Europe with North American companies looking to outsource software development.

This model worked exceptionally well as EPAM was able to offer high-quality software developers at a fraction of the cost of their US counterparts.

However, with the bulk of their workforce based in Ukraine, the Russia-Ukraine war put a major dent in operations starting in 2022. Thankfully, EPAM was able to successfully relocate most of their employee-base, resume operations, and reaccelerate growth.

Now, however, they’re facing a new headwind (or at least a perceived headwind) from the rise of tools like Claude Cowork and OpenAI Codex.

EV/EBIT: 10.1x

5yr Revenue CAGR: 15.5%

Just like the rest of the consulting and research sector, Gartner has been deemed yet another AI casualty by Mr. Market.

For many IT professionals, Gartner is the go-to source for the latest industry insights. With more than 2,400 experts, Gartner is able to produce high quality research that covers many different industries and serves over 13,000 clients. However, as AI has reduced the time and effort required to pull together information, customers are starting to push back against Gartner’s multi-year, upfront subscription pricing model.

We’re now seeing this pushback show up in the financials as last quarter, Gartner reported just 2% revenue growth, which is their slowest rate in a decade (excluding COVID).

EV/EBIT: 11.7x

5yr Revenue CAGR: 9.1%

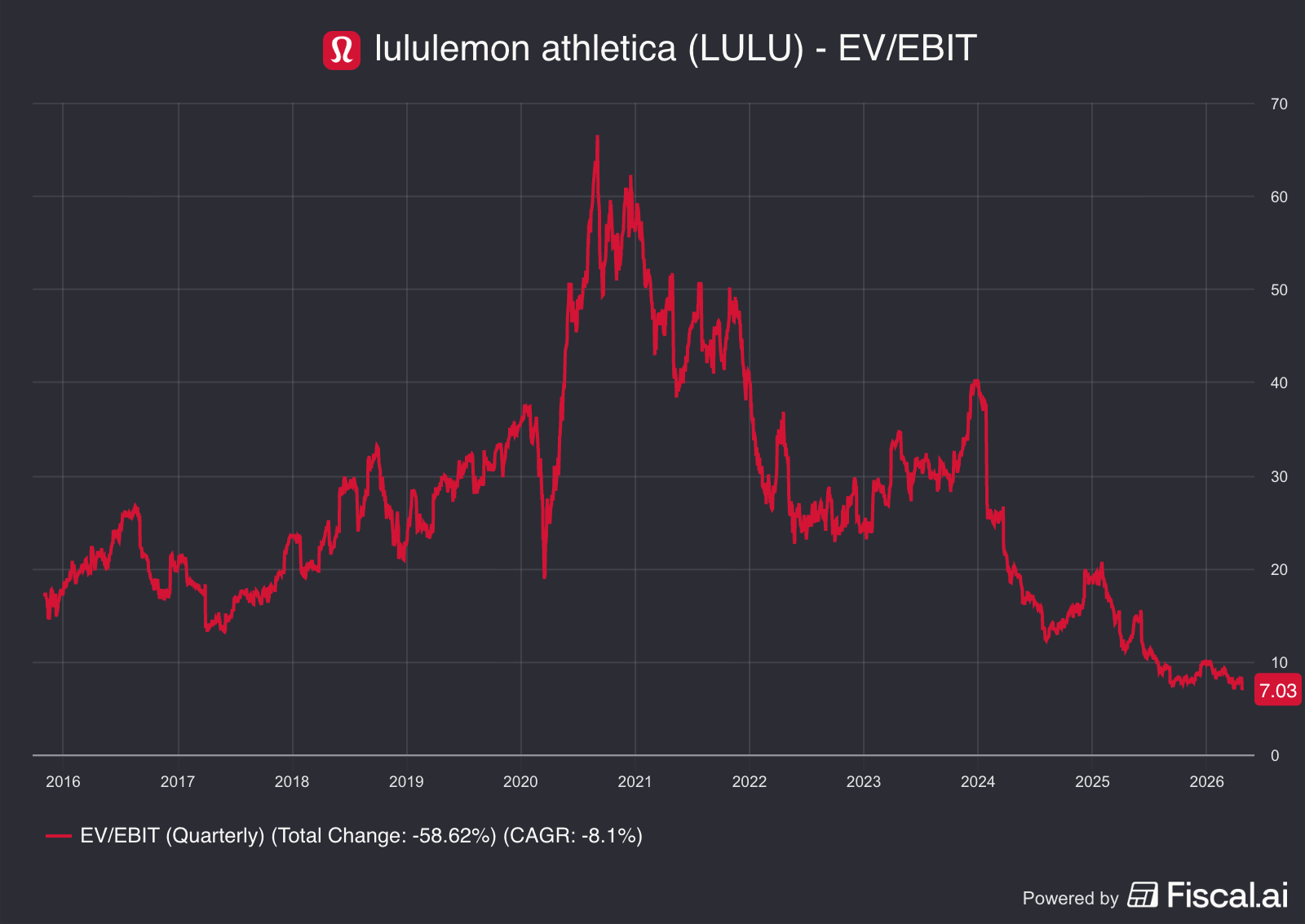

Lululemon is a perfect example of why investing in apparel can be so challenging.

Lululemon essentially pioneered the entire “athleisure” category. From 2005 to 2025, they grew revenue by 32% annually, earnings per share by 42% per year, they expanded store count from 25 to 767, and they successfully expanded across several international markets.

Yet… the stock is flat over the last 8 years.

Competition from the likes of Alo, Athleta, Vuori, Gymshark, and many other new brands have resulted in Lululemon reporting negative same store sales growth in America over the last 2 years.

To make matters worse, now former CEO Calvin McDonald unexpectedly resigned in January 2026. To fill the role, lululemon’s board appointed Heidi O’Neill this week, a 25 year Nike veteran. Investors don’t seem ecstatic about the new hire (stock dropped 12% this week) as Heidi comes from Nike, which is facing significant brand problems of their own.

EV/EBIT: 7.03x

5yr Revenue CAGR: 19.4%

Software and consulting seem to be the two industries that have lost the market value due to AI. And Cognizant Technology Solutions would be one of those consulting casualties.

Cognizant operates a classic IT consulting model that charges clients primarily based on “billable hours”. As AI enables developers to be more productive and efficient, clients will likely expect Cognizant’s billable hours to shrink.

While Cognizant’s management team believes this AI wave will be a net-new tailwind for the business and will encourage more clients to turn to them, investors don’t seem to buy the hype yet. Despite averaging 6% annual revenue and EPS growth over the last decade, and reaccelerating revenue growth in 2025, Cognizant is currently trading at its cheapest valuation in a decade.

EV/EBIT: 7.8x

5yr Revenue CAGR: 4.9%

That’s all for this week.

If you have any questions about Fiscal.ai or any feedback for the newsletter, feel free to reply to this email!