- Fiscal.ai

- Posts

- 🗞 Luxury Hangover? Inside the Industry's Sudden Collapse

🗞 Luxury Hangover? Inside the Industry's Sudden Collapse

What happened to luxury stocks?

Braden Dennis & Ryan Henderson

March 29, 2026

Written by: Ryan Henderson & Braden Dennis

Happy Sunday! 👋

Today we’re taking a look under the hood at the sudden collapse of the luxury industry.

Let’s dive in!

Featured Story

Luxury Hangover? Inside the Industry's Sudden Collapse

For the better part of the last two decades, luxury was the place to be.

A growing upper-class drove greater volumes, brands consistently raised prices, and profit margins expanded.

But starting around 2023/2024, cracks started to show.

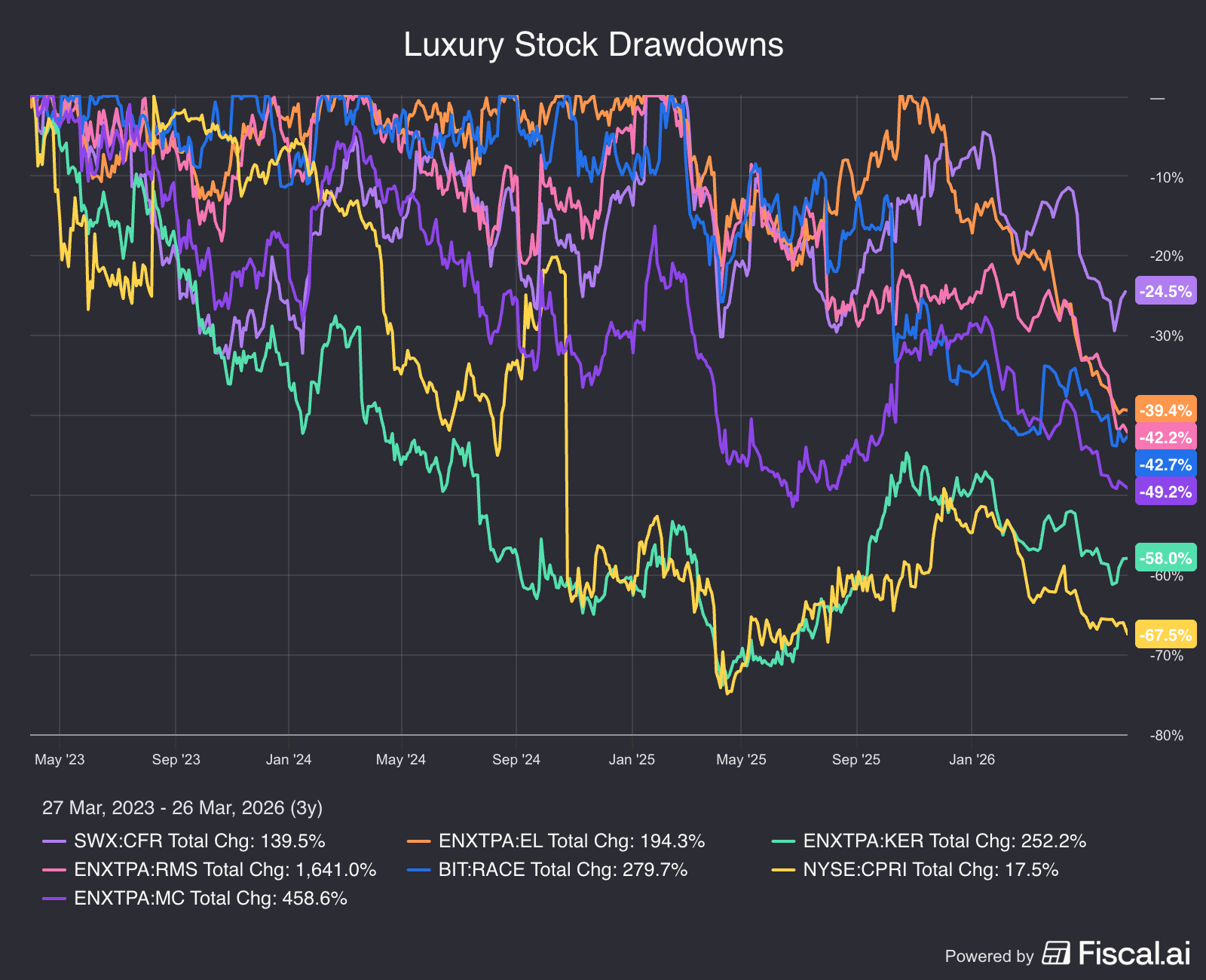

And now, the entire industry is in a severe drawdown.

Richemont: -25%

EssilorLuxottica: -39%

Hermès: -42%

Ferrari: -43%

Prada: -45%

LVMH Moët Hennessy: -49%

Kering: -58%

Capri Holdings: -67%

“Luxury” has long been considered one of the most recession-proof industries in the world.

By catering to the world’s most affluent, these prestigious brands were — at least in theory — immune to general economic downturns.

But in 2025, that narrative broke.

For the first time since the 2008 financial crisis (excluding the pandemic), the luxury industry reported overall revenue declines.

What went wrong?

There have been several global headwinds over the last few years that have muddied the operating environment for luxury brands. The US 2022 interest rate hike cycle, geopolitical tensions damaging consumer confidence, tariffs pricing out aspirational customers.

But above all else, it seems there’s one market in particular putting a dent in financial results: China.

Case Study #1: LVMH

LVMH (Moët Hennessy Louis Vuitton) is the largest luxury company in the world by market cap. Home to brands like Louis Vuitton, Christian Dior, Tiffany & Co., Sephora, Bulgari, and dozens more, you could perhaps group LVMH into the “aspirational luxury” bucket.

That is to say, the price tag on LVMH products isn’t so high that it remains unattainable to middle-class customers. To put some numbers on it, the average Louis Vuitton bag costs somewhere in the range of $2,000-$3,000, whereas an Hermès Birkin bag will cost $10,000 minimum (if they even let you buy one).

While this focus on aspiring luxury customers certainly widens the addressable market, it also creates more economic sensitivity for LVMH.

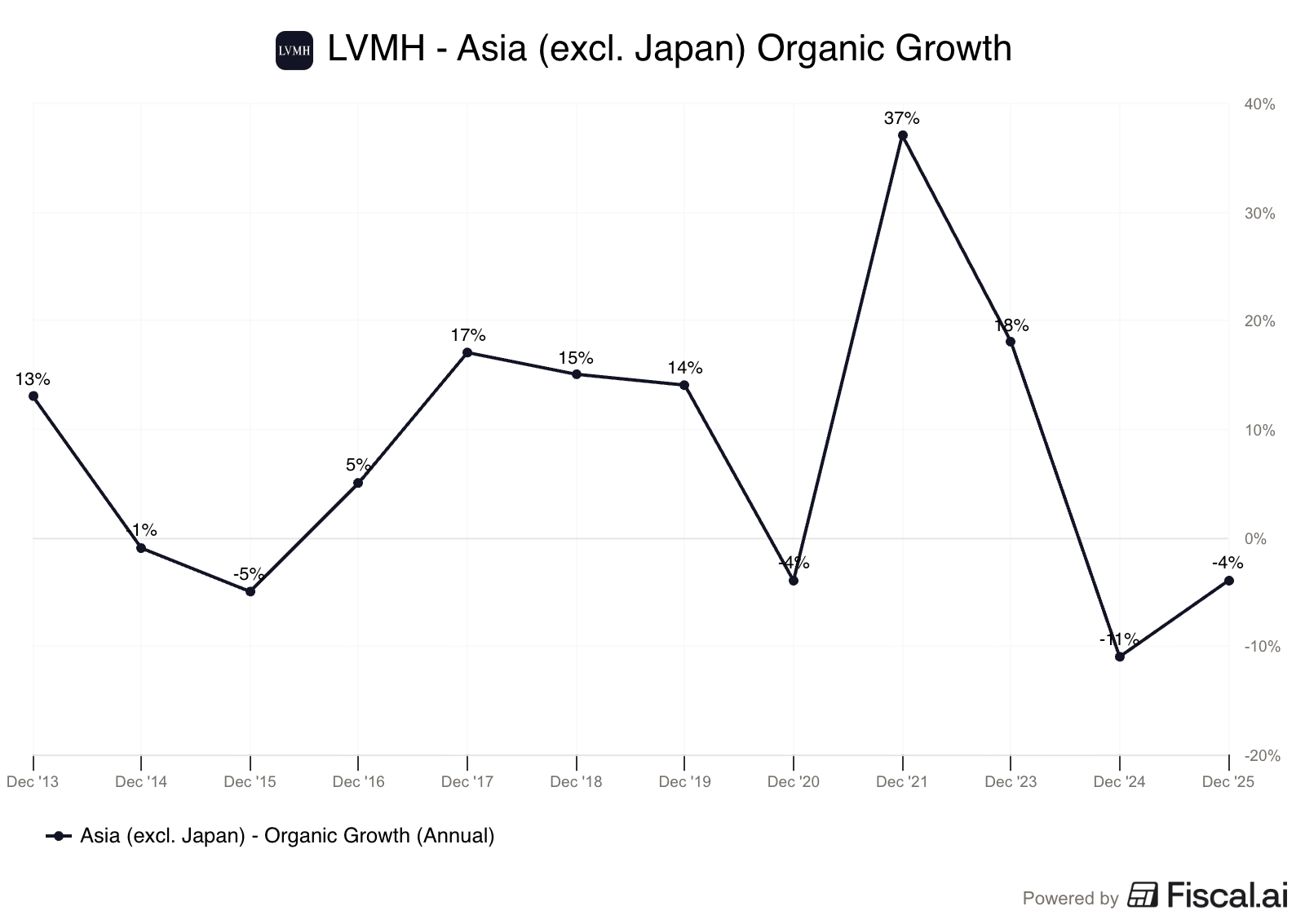

This became evident over the last couple of years. Following the pandemic, China was on pace to become the world’s largest luxury market, and by the end of 2022, Asia (excluding Japan) was LVMH’s largest revenue contributor accounting for 30% of overall revenue.

However, as a property crisis emerged in China and youth unemployment hit record highs, consumer confidence began to weaken, and LVMH felt the repercussions.

Lapping the post-pandemic boom, LVMH reported two consecutive years in a row of negative organic growth in China.

Case Study #2: Ferrari

Ferrari is about as “luxury” as luxury gets.

To paint a picture, the average operating margin in the auto industry is ~3.9%. Ferrari, on the other hand, generates 30% operating margins.

By virtually any criteria, Ferrari has a phenomenal business model. The allure to own a Ferrari is so strong that the company has to be highly selective over who they let buy their vehicles. Typically, a wannabe customer has to demonstrate a longstanding history of prior ownership through used vehicles to even earn the “privilege” to buy one new.

This dynamic has created phenomenal pricing power for Ferrari. The average Ferrari sells for north of €400,000, and that figure has grown by 5.2% a year since 2012.

To pair with that pricing power, Ferrari has historically increased shipments by just 3%-4% a year on average. That limited shipment growth is very much intentional, and is at the core of Ferrari’s scarcity-focused model.

“Ferrari will always deliver one car less than the market demands.”

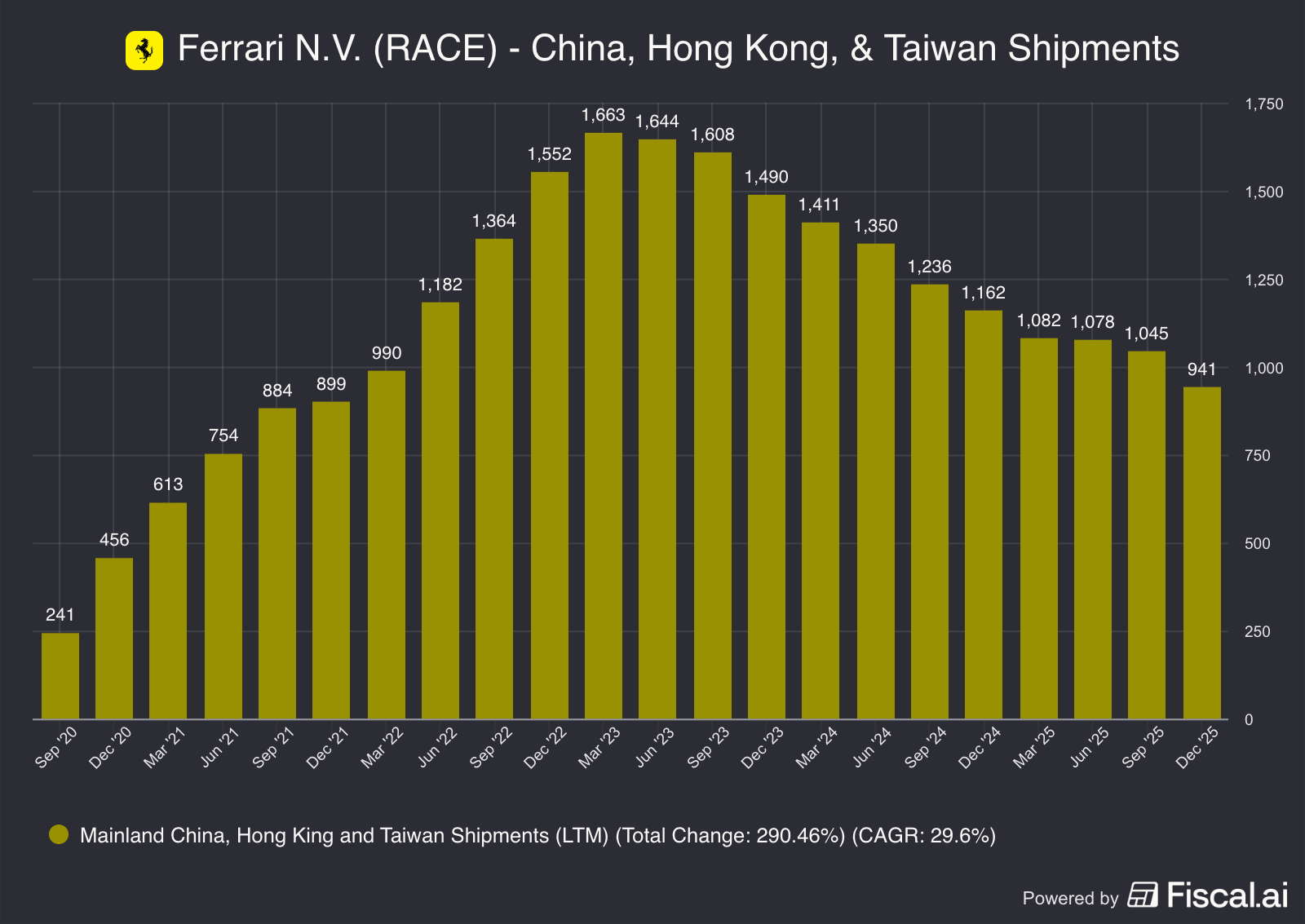

From 2019 to 2023, shipment growth accelerated to 7.8% annually. The fastest growing market over that timeframe? China.

Combined with Ferrari’s pricing power, this created an acceleration in revenue growth, and in turn, investors rewarded Ferrari with multiple expansion.

However, even Ferrari — the company that is supposed be one of the most resilient against general economic weakness — is seeing a slowdown in shipments. In fact, for the first time in more than a decade (ex. the pandemic), Ferrari reported an annual decline in shipments for 2025.

And the largest contributor to those declines? Again, China.

Shipments to Mainland China, Hong Kong, and Taiwan are now down 43% from their 2023 peak. Excluding this market, Ferrari would have grown shipments in 2025.

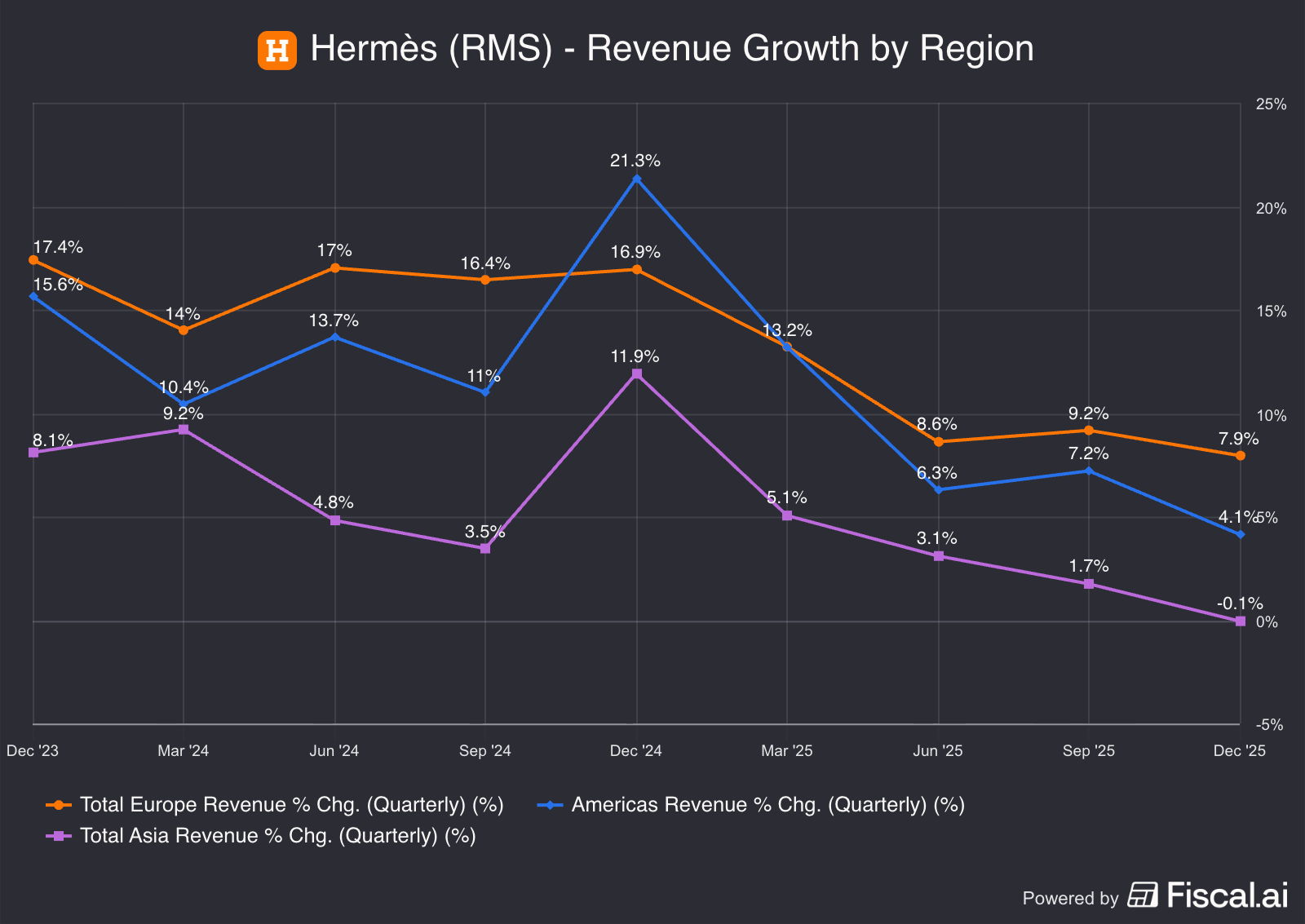

Case Study #3: Hermès

Hermès is one of the most prestigious luxury brands in the world.

Like Ferrari, Hermès thrives on scarcity and exclusivity. Their popular Birkin Bags, which are each handcrafted by French artisans, retail anywhere from $10,000 to $300,000.

These exorbitant price points are what enables Hermès to generate a whopping 42% operating margins. For reference, LVMH generates about half that at 22% operating margins.

While Hermès is yet to experience an actual overall revenue decline in the same way that LVMH has, revenue growth from Asia specifically has turned negative in reported currency. This marks the slowest growth Hermès has seen in Asia in more than a decade.

Although Hermès’ financial results have held up better than most other luxury companies, the Asia (excl. Japan) geography — which is primarily comprised of China — is the company’s largest revenue contributor. With concerns over the prolonged contraction continuing in China, shares of Hermès have dropped by 42% from highs and the company now trades at its cheapest valuation in more than 5 years.

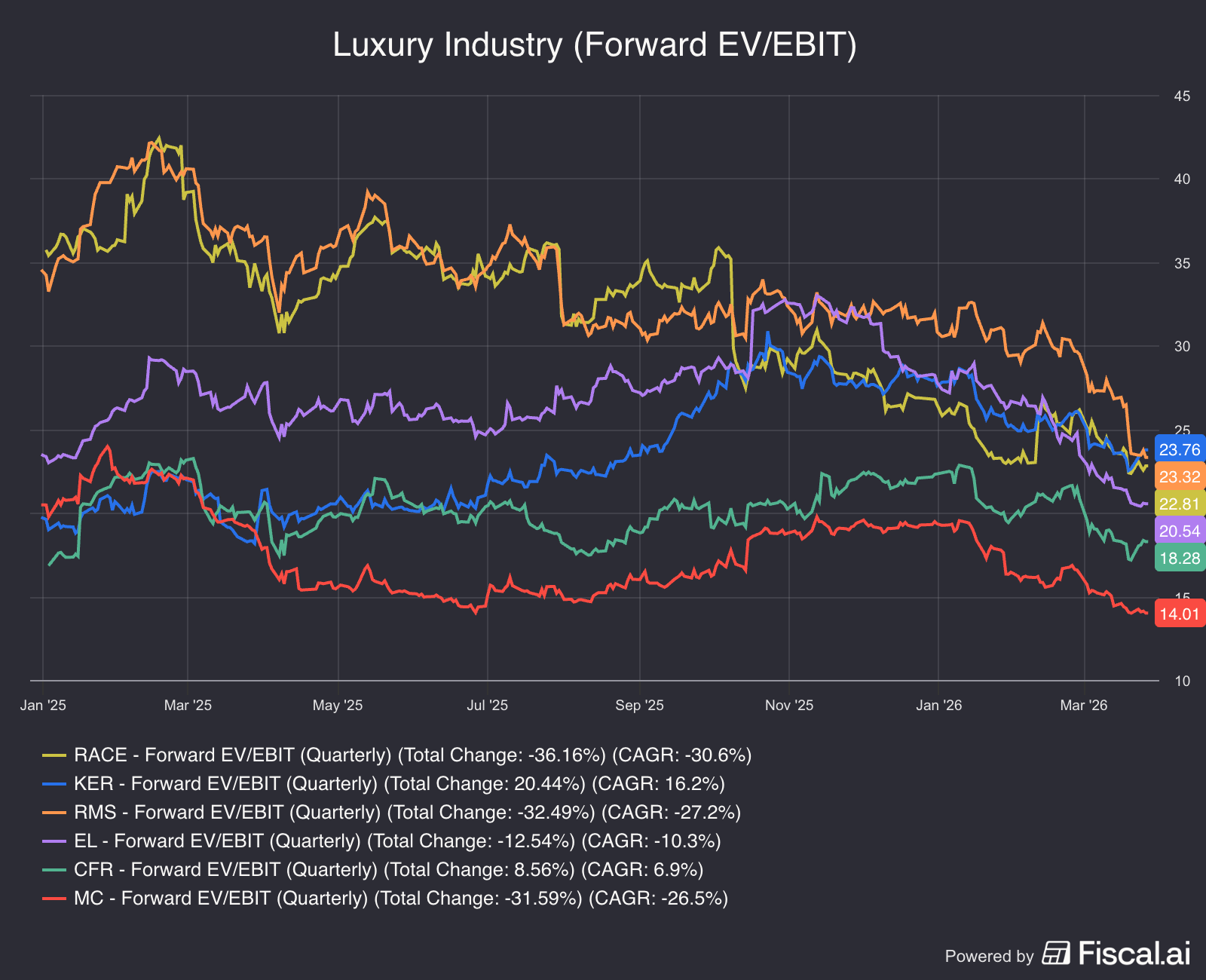

Valuations Today:

For investors looking to go bargain hunting, many luxury companies are trading at their cheapest valuations in years.

That’s all for this week.

If you have any questions about Fiscal.ai or any feedback for the newsletter, feel free to reply to this email!